Introduction: What is Section 80TTB?

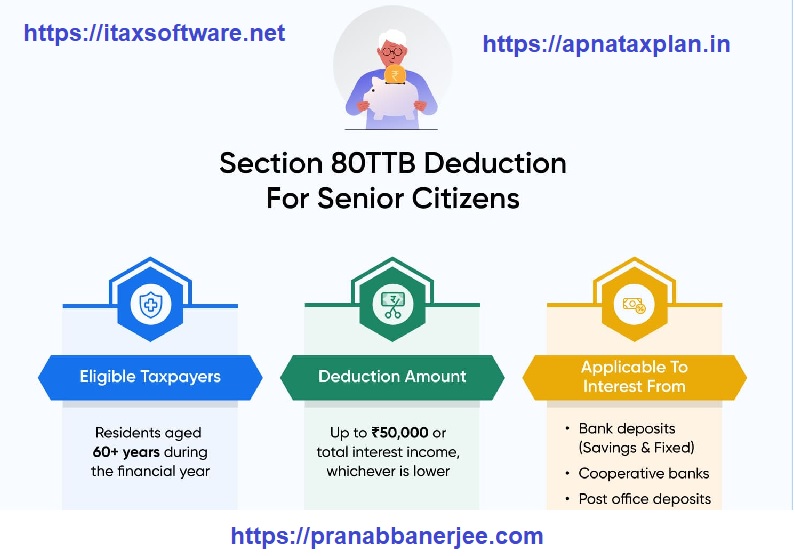

Section 80TTB, introduced in the Union Budget 2018, is a beneficial provision under the Income Tax Act, 1961 designed exclusively for senior citizens aged 60 years or above. This section offers a deduction of up to ₹50,000 on interest income earned from savings accounts, fixed deposits (FDs), and recurring deposits (RDs) maintained with banks, post offices, or cooperative societies.

The government recognised that retirees often rely heavily on fixed-income sources like bank deposits. Hence, Section 80TTB was introduced to ease their tax burden and ensure financial security during retirement. Unlike Section 80TTA, which caters to non-senior citizens, Section 80TTB provides enhanced relief for elderly taxpayers.

Why Section 80TTB Matters for Senior Citizens

Transitioning into retirement often means shifting from active income to passive income. Most senior citizens depend on interest earnings from savings and deposits to meet day-to-day expenses. Recognising this, Section 80TTB becomes crucial as it:

- Reduces taxable income, offering direct tax relief.

- Encourages financial discipline by promoting safer savings options.

- Improves liquidity, enabling better management of healthcare and living costs.

In short, this section promotes economic independence and financial dignity for senior citizens.

Eligibility Criteria for Claiming Section 80TTB Deduction

To claim benefits under Section 80TTB, taxpayers must satisfy specific conditions.

- Resident Status: Only resident senior citizens are eligible. Non-resident Indians (NRIs) cannot claim this deduction.

- Age Requirement: The taxpayer must be 60 years or older at any time during the financial year.

- Source of Income: The deduction applies solely to interest earned from deposits in:

- Banks (savings, fixed, or recurring deposits)

- Post offices

- Cooperative banks or societies

If these conditions are met, the individual can avail up to ₹50,000 in deductions annually.

Amount of Deduction Allowed Under Section 80TTB

The maximum deduction available under Section 80TTB is the lower of:

- ₹50,000, or

- The total interest earned from eligible deposits.

For instance:

- If a senior citizen earns ₹45,000 as interest, they can claim the entire ₹45,000.

- If they earn ₹60,000, the deduction is capped at ₹50,000.

This clear structure simplifies tax planning and ensures that retirees can manage their income effectively without unnecessary complexity.

Key Exceptions Under Section 80TTB

Although Section 80TTB provides generous relief, certain types of interest income are not eligible:

- Deposits held on behalf of others, such as firms or AOPs.

- Interest from corporate bonds or debentures.

- Deposits under the new tax regime (Section 115BAC), as this regime disallows most deductions, including 80TTB.

Therefore, senior citizens should opt for the old tax regime if they wish to maximise deductions like 80TTB.

Difference Between Section 80TTA and Section 80TTB

| Particulars | Section 80TTA | Section 80TTB |

| Eligible Taxpayers | Individuals and HUFs (below 60 years) | Senior citizens (60 years or older) |

| Eligible Income | Interest from savings accounts only | Interest from savings, fixed, and recurring deposits |

| Deduction Limit | Up to ₹10,000 | Up to ₹50,000 |

| Availability | All eligible taxpayers | Exclusively for senior citizens |

| Applicable Deposits | Savings accounts | Savings, FD, and RD accounts |

This table clearly highlights that Section 80TTB provides broader coverage and higher deduction limits, making it far more beneficial for senior citizens than 80TTA.

Example of Tax Savings Under Section 80TTB

Let’s take an example to understand the practical savings:

Scenario:

Mrs. Sharma, a 65-year-old resident, earns:

- Savings interest: ₹6,000

- FD interest: ₹1,50,000

- Other income: ₹1,00,000

| Income Type | Non-Senior Citizen | Senior Citizen (with 80TTB) |

| Savings Interest | ₹6,000 | ₹6,000 |

| FD Interest | ₹1,50,000 | ₹1,50,000 |

| Other Income | ₹1,00,000 | ₹1,00,000 |

| Gross Total | ₹2,56,000 | ₹2,56,000 |

| Deduction (80TTA/80TTB) | ₹6,000 | ₹50,000 |

| Taxable Income | ₹2,50,000 | ₹2,06,000 |

➡️ Result: Mrs. Sharma saves ₹44,000 in taxable income just by using Section 80TTB.

Documents Required for Claiming the Deduction

Senior citizens don’t need extensive paperwork. They should, however, maintain:

- Bank or Post Office Interest Certificates

- PAN Card

- Form 16/26AS (for TDS verification if applicable)

These documents ensure smooth processing and reduce the chances of errors during ITR filing.

Section 80TTB in the New Tax Regime

Under the new tax regime (Section 115BAC), introduced in FY 2020–21, taxpayers enjoy lower slab rates but cannot claim most deductions, including Section 80TTB.

Hence, before choosing between the old and new tax regimes, senior citizens must compare tax liability under both. In most cases, those earning higher interest incomes benefit more from the old regime, thanks to deductions like 80TTB, 80C, and 80D.

Benefits of Section 80TTB for Senior Citizens

- Higher Tax Relief: Offers five times more deduction than Section 80TTA.

- Encourages Safe Savings: Promotes risk-free investments in deposits.

- Better Financial Planning: Reduces taxable income, increasing post-tax returns.

- Simplified Compliance: Easy to claim and verify through bank statements.

- Empowers Senior Citizens: Enhances financial independence and comfort.

Step-by-Step Guide: How to Claim 80TTB Deduction in ITR

- Calculate Interest Income: Gather interest details from all bank and post office accounts.

- Declare Under “Income from Other Sources.”

- Enter Deduction Under Section 80TTB: Mention up to ₹50,000 or actual interest earned.

- Verify Details: Cross-check with bank statements or Form 16A.

- Submit the ITR: Once verified, submit the return to complete the process.

This simple approach ensures accuracy and maximises deductions.

Practical Tax Planning Tips for Senior Citizens

- Always prefer cumulative deposits to earn higher interest.

- Compare the old vs the new tax regime before filing.

- Keep a record of TDS deductions to prevent double taxation.

- Consider using automatic tax calculators in Excel for accuracy.

- Diversify deposits between banks and post offices for safety and returns.

Common Mistakes to Avoid While Claiming 80TTB

- Declaring gross interest without deducting TDS.

- Claiming 80TTB under the new tax regime.

- Including non-eligible interest (e.g., corporate bonds).

- Failing to retain bank interest certificates for proof.

Avoiding these mistakes ensures hassle-free ITR filing and maximum benefit.

FAQs on Section 80TTB of the Income Tax Act

Q1. Can a senior citizen claim both Section 80TTA and 80TTB?

No. If 80TTB is claimed, 80TTA cannot be availed simultaneously.

Q2. Is interest from recurring deposits eligible under 80TTB?

Yes, interest from RDs is eligible if held in banks, post offices, or cooperative societies.

Q3. Are NRIs eligible for this deduction?

No. Only resident senior citizens can claim it.

Q4. What happens if the total interest exceeds ₹50,000?

You can only claim a maximum deduction of ₹50,000 under this section.

Q5. Can senior citizens under the new tax regime claim 80TTB?

No. The deduction applies only under the old regime.

Q6. What if multiple bank accounts are held?

The total interest from all accounts must be aggregated before applying the deduction limit.

Conclusion: Financial Freedom Through Section 80TTB

Section 80TTB is more than just a tax relief; it’s a financial safeguard for India’s elderly. By offering up to ₹50,000 in deductions, it reduces tax liability and promotes secure savings habits.

Senior citizens who rely on interest income can benefit immensely from this provision—especially under the old tax regime. Understanding its scope, limits, and procedure allows retirees to enjoy their golden years with greater financial peace.